Is there a market for less capable AI models?

A competitor of OpenAI and Anthropic needs paying customers to survive. Will they exist?

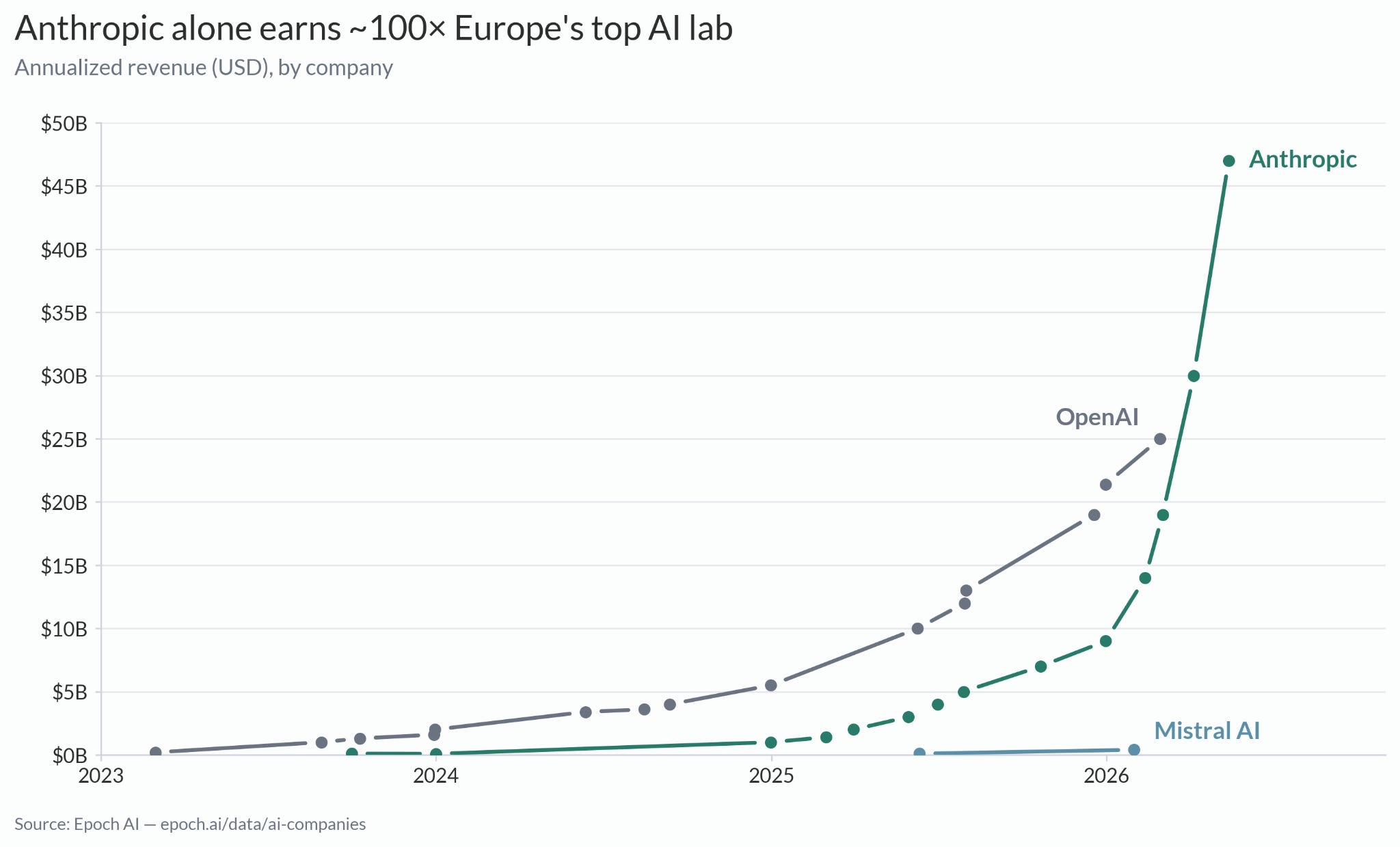

Artificial intelligence companies make a lot of money. Revenue in the sector is growing almost ten times a year, from $560 million per month early 2025 to $5 billion per month today.

But this revenue is almost entirely attributable to two American companies: OpenAI and Anthropic. Mistral reported earlier this year that its annual revenues had reached $400 million, around the same time that Anthropic’s annual revenue reached $9 billion. Since then, Anthropic’s revenue has grown fivefold, to $47 billion; Mistral has not yet released new figures.

Whether this distribution persists matters a lot. It determines who will make money off AI, and who can afford to stay at the frontier. AI progress is expensive. Whether privately or publicly funded, AI projects that cannot generate revenue will fall behind.

In this post, we’ll look at two questions:

1. Why is AI revenue so concentrated?

2. Will frontier companies stay ahead?

Why is revenue so concentrated?

In many industries, the best workers make much more than normal workers: the best football players and musicians make thousands of times the industry average; in AI research, the best engineers earn tens of millions of dollars.

These sectors are governed by what Sherwin Rosen called the economics of superstars, which apply if two conditions are true: imperfect substitution and joint consumption. Imperfect substitution means that quantity cannot replace quality: several bad violinists cannot substitute for one great violinist, and a thousand bad lawyers are not equivalent to one good lawyer. Joint consumption means that the same product can be consumed by everyone at once: a single producer can serve the entire market cheaply (think recordings, software, or Substack posts). If both conditions hold, you get superstar returns.

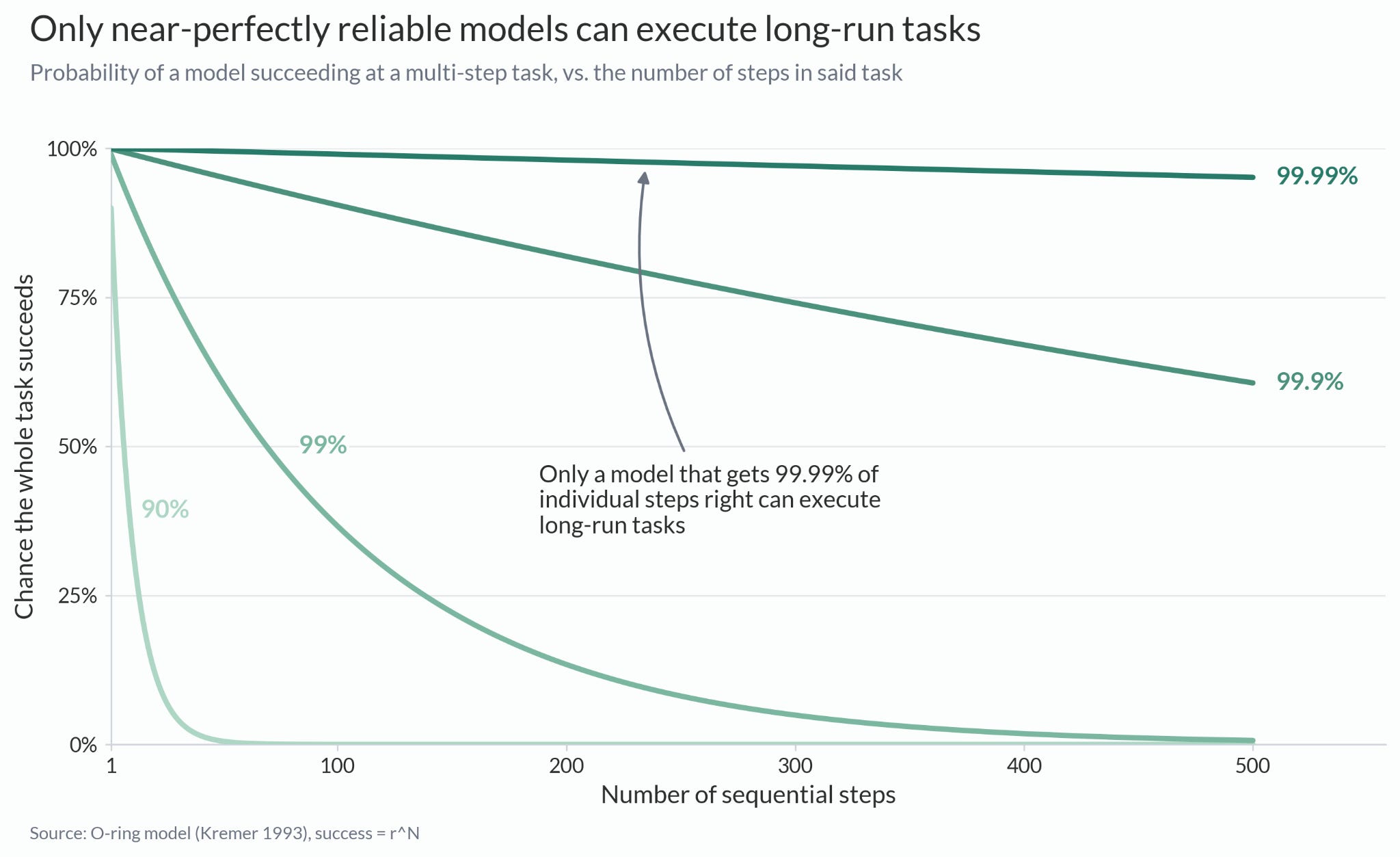

Both conditions appear to apply to AI. You cannot use multiple instances of a weaker model to approximate the output of a stronger model. New models can also solve new problems, because they can put together hundreds of individually correct decisions. Worse models are more error-prone, which puts hard problems entirely out of reach for them. It took GPT 5.6 to solve a fresh Erdős problem; no amount of GPT-4o instances would have been able to do the same.

New models can also do existing tasks to a standard that no combination of weaker models can match, similarly to how many people can write books or compose music, but no committee could write War and Peace or come up with Bach’s cantatas.

For such tasks, people appear to prefer the better model. Consider emails or job applications. We do not know any believer in the commoditization thesis who is using Kimi 2.5 or Le Chat to help with these simple administrative tasks, despite both being capable enough to do them.

One explanation is switching costs: the effort of choosing different models for different tasks is not worth it when the cost of prompting a more expensive model under a subscription is zero. For companies with more sophisticated processes (and usage-based API bills), switching costs will feature less heavily.

But such businesses might also prefer better models for simple tasks for a different reason. Many things in business and life have nonlinear outcomes: a slightly better sales pitch can win a contract; a slightly better trade is the difference between making and losing millions; and a slightly better job application is the difference between getting and not getting a job. In areas where a small (relative) edge in performance makes the difference between winning and losing, the better model or worker is worth all of the upside it creates.

Sherwin Rosen’s joint consumption condition is a bit trickier. In traditional software, one person using a computer program has no effect on someone else using that program, so everyone can use the best. AI is somewhat different. One person using a model’s weights (its design) has no effect on someone else using those weights, but someone using an AI company’s API does exclude others from using it, because the compute the model runs on is itself scarce even when the model is not. The result we’d expect to see is fragmentation on the compute layer, with many different providers hosting models, and concentration on the model layer, as everyone switches to hosting the best model at a given time.

Will frontier companies stay ahead?

For the economics of superstars to persist, Anthropic and OpenAI must remain better than the competition. Their models currently being better gives them much deeper pockets: Anthropic makes $47 billion per year and recently raised another $65 billion to train future models. Many companies experience economies of scale when spending money on research: a large company can spread fixed research costs over a much bigger revenue base, while an upstart has to cover those same costs with far less. This was one source of Intel’s long-term dominance, and it is what underpins ASML’s monopoly on extreme ultraviolet (EUV) lithography machines.

But eventually, each additional dollar spent on research should achieve less, allowing other companies to catch up – as happened to Intel, and as may happen to ASML.

ASML and Intel were limited, however, by what kinds of increasing returns they had. EUV machines make them lots of money, but the act of owning EUV machines does not itself make ASML better at discovering better EUV machines. In this sense, AI is different: it can write code, come up with experiments, and implement them. It is uniquely capable of improving itself. (The only other example we can think of is this lathe, which is necessary for making lathes.)

Anthropic is able to use its models for internal AI research where its competitors cannot. One of the reasons we have heard from a friend at DeepMind for the talent flight to Anthropic is precisely this: that DeepMind researchers feel stunted without access to a good internal model. When Anthropic did finally release their strongest model to the public, they made it useless for AI research.

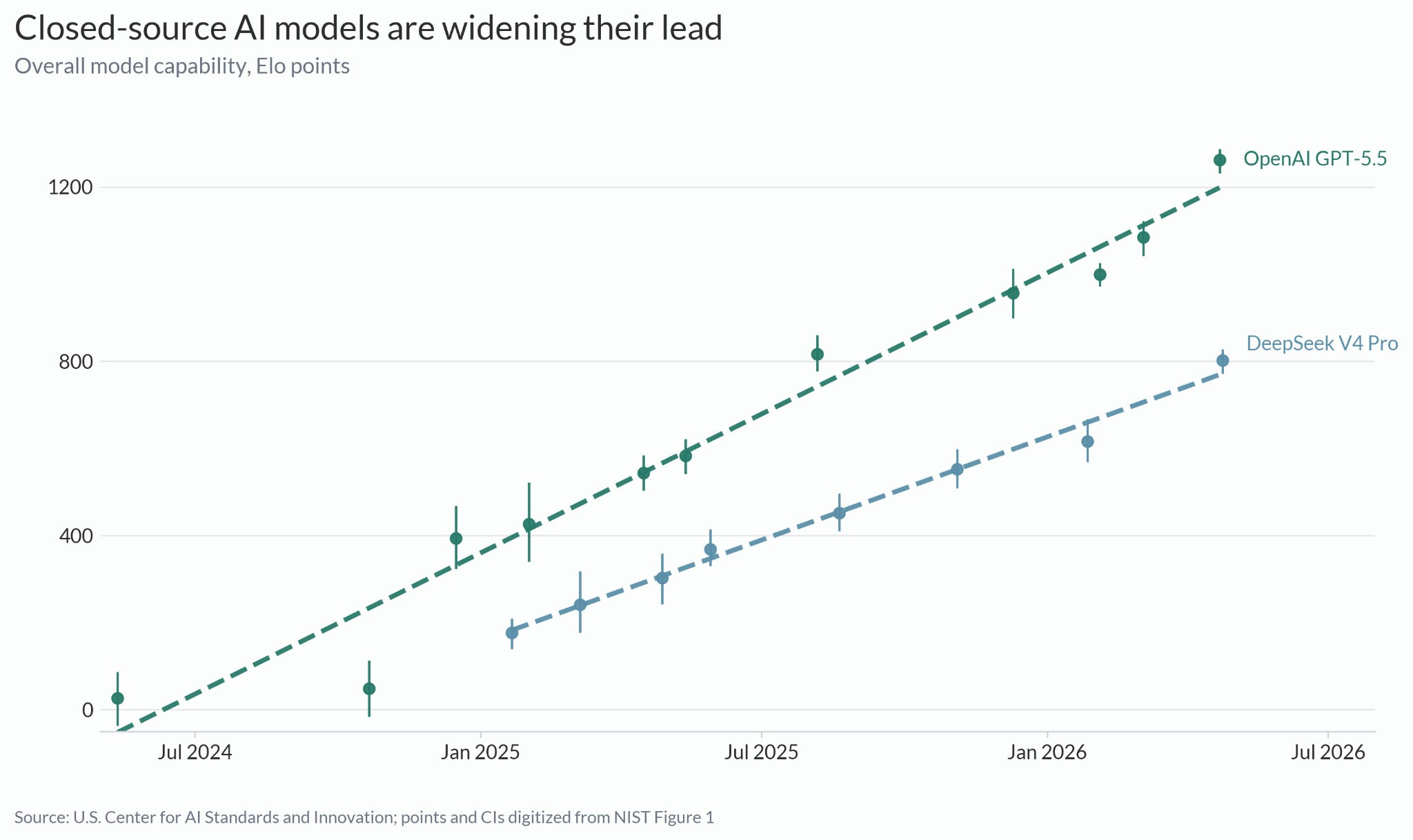

Today, the best AI companies are pulling away from their competitors. xAI is leasing its data centers to Anthropic rather than using them itself, Google DeepMind is losing its superstars to Anthropic, and Meta is spending tens of billions and struggling to produce a good model.

The same is true for cheap Chinese models. They have stayed somewhat close to the frontrunner but are falling behind over time. Last year, the best Chinese companies were only six months behind the best American companies; now, that gap has grown to eight to ten months.1

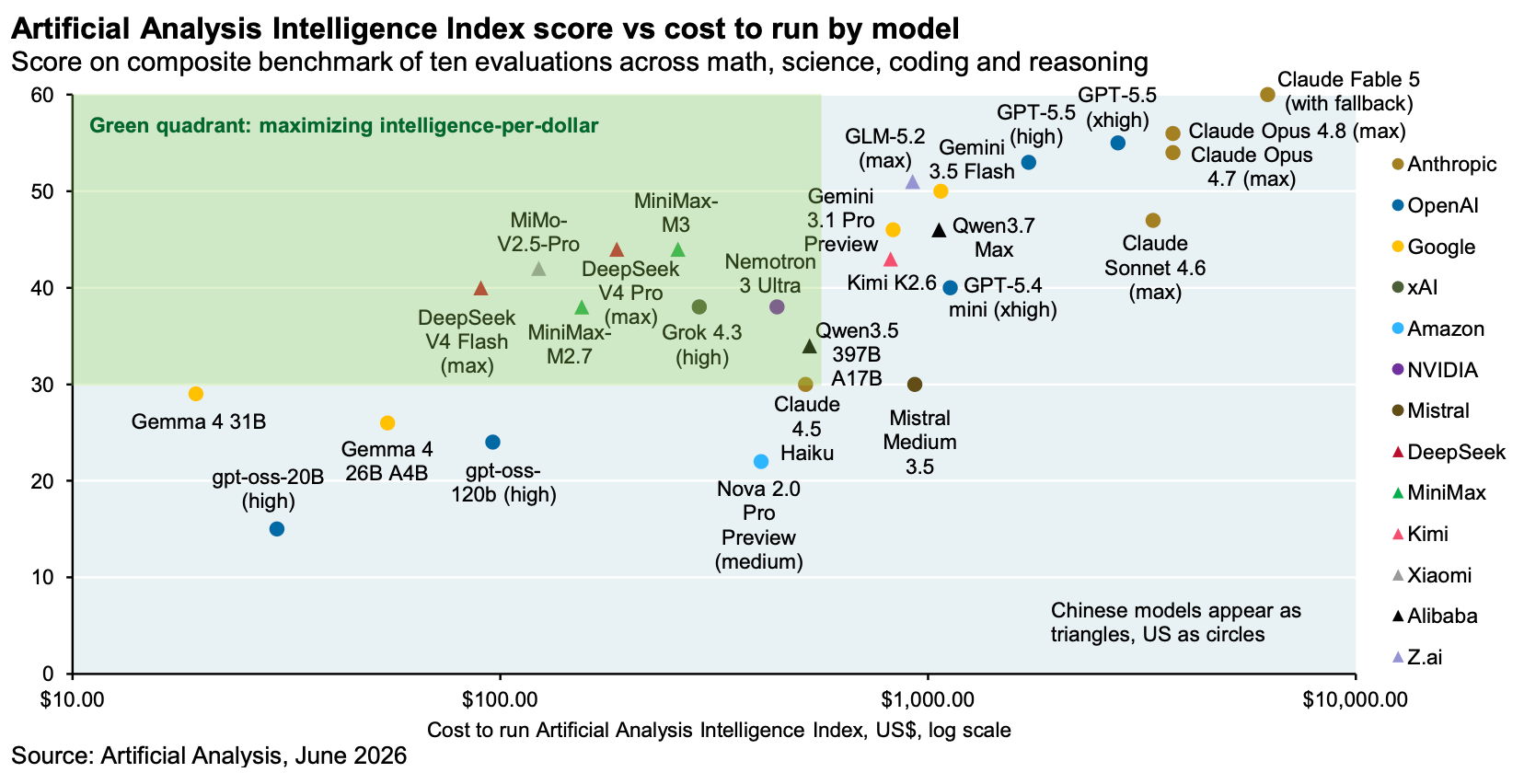

This is a consequence of how they are made. Many Chinese models are distilled from American models, trained on input-output combinations of Anthropic and OpenAI products. GLM-5.2, the best Chinese model, was so heavily trained on Claude Opus output that it frequently believes it is Claude. But distillation necessarily involves some loss along the way, meaning you cannot surpass the frontrunner. Distillation is also becoming less effective, as Anthropic and OpenAI clamp down on distillation attacks and the underlying intelligence of good models transfers increasingly poorly. (For European companies, distillation probably isn’t even politically viable, given that American companies treat it as a deeply adversarial action.)

The other problem for open-source progress is that open-source companies don’t make much money. Companies that serve open-source models, like Baseten and Fireworks AI, are making money. But the companies that created the models don’t capture any of that value. Making better AI models is expensive, and it is not clear why any provider beyond Meta and TikTok, which have a different channel to make money from models, would perpetually provide them for free, let alone surpass the frontrunners.

OpenAI and Anthropic might not be able to sustain the current speed of improvement. But a slowdown doesn’t seem like the likeliest outcome, given the enormous amounts of additional compute soon coming online, and the fact that the leading labs are only now beginning to effectively use internal models to accelerate AI research.

Cheap models might provide an alternative for easy or unimportant tasks. But even that wouldn’t change much about the revenue distribution between AI companies: once a task can be done by a commodity model, its price collapses. The revenue from this kind of work is small even if it creates lots of the value. In this world, the AI market would resemble something like the market for lawyers, where much work is routine and modestly paid, while a few superstars work on high-value problems and make enormous returns.

The consequences of revenue concentration

At some point in the future, a French or German company may release a good AI model that is only slightly worse than what is made by Anthropic or OpenAI. This model would provide temporary independence.

But a model that is close to the frontier one month will be far behind it six months later. To stay a fixed distance behind the frontier, the model would need constant improving. To fund that improvement, the model would have to make money.

Quite a bit of capital is being invested in companies that are developing or serving models behind the frontier: Mistral has raised at an €11.7 billion valuation, Baseten at $13 billion, Fireworks at $4 billion, and AMI Labs at €900 million. It is fine for private investors to take these risks. It is different when European governments, or those advising them, assume that there is a great opportunity being left on the table here.

To justify government investment, there must be some benefit that the market is not pricing in. That benefit may be national security. But if it is national security, then we should be clear-eyed about the fact that it is governments who will pick up most of the tab. Without financial returns and especially without distillation, staying even a fixed distance behind the best models will be achievable only with exponentially growing subsidies.

Epoch’s Capabilities Index (ECI) is showing a narrower gap. But ECI is heavily dependent on widely known benchmarks, and Chinese open-source models are much more optimized toward benchmarks than OpenAI’s or Anthropic’s models.

| A guest post by

|

This piece provides a brilliantly clear economic lens on why the AI market is not commoditizing the way many predicted. Applying Sherwin Rosen's "economics of superstars" to AI perfectly explains the massive revenue concentration we are seeing with Anthropic and OpenAI. The point about imperfect substitution is especially sharp. You truly cannot stack a hundred mediocre models to solve a frontier level problem, and your observation that a slightly better output creates nonlinear business value perfectly explains why even simple tasks migrate to the best available tools.

Your conclusion regarding the inevitable need for exponentially growing government subsidies for sovereign AI raises a critical issue. Given this reality, do you foresee a future where non US nations are forced to pool their resources into international consortia just to stay in the race, or will they eventually have to capitulate and build their national security infrastructure entirely on American APIs?

I explore very similar structural shifts, focusing specifically on how these AI market dynamics and technological leaps impact community management and the future of our digital spaces. If you are open to exchanging ideas and growing together, I would love for you to check out my space: https://nicolocaiti.substack.com

Great post! I'm surprised so few people have really considered the long term viability of OS models given how quickly they are burning models.

You mentioned that one big difference with Rosen's superstar model that we see in law, tech and other domains is the potential for RSI that might actually keep revenue even more concentrated. One point of divergence from this allegory is that unlike with lawyers or footballers, you can reasonably expect a comparable performance from a much cheaper alternative in the near future. The implication of the Chinese labs being 8-10 months behind is that by the end of the year, everyone will be able to access a cheap, open source Mythos-level capability.

If there is some kind of diminishing return of having a more performant model or there exists some significant set of async applications AIs aren't worth the cost right now (but will be in a few months) then it's easy to imagine a much bigger role for OS models and slim profits going forward. Intelligence is an exponentially depreciating IP, without exponential increases in performance from scaling laws or RSI or something else there isn't much point in frontier labs.

Summary of my thoughts:

If just diminishing returns -> Within a few years intelligence is free from OS providers

If just RSI -> Frontier labs pull away from everyone and we are in the singularity

If RSI and diminishing returns -> Frontier labs may hold their lead for a while but diminishing returns are more strongly exponential and the timeline to reach abundant intelligence is just longer

If neither -> Not clear, if markets can keep underwriting the compute cost and the models continue to scale exponentially then we might end out in a superstar model again.